Two days on from the prime minister’s announcement, the size of the economic package is already down to Rs 14.53 lakh crore

The government is telling us it has come up with a Rs 20 lakh crore economic package to rescue the economy from the negative impact of Covid-19. This so-called Rs 20 lakh crore package also includes economic announcements which were the decisions of the Reserve Bank of India.

What does this mean? In weak economic environments, any central bank tries to flood the financial system with cheap money by lending to banks at a low interest rate. The hope is that the banks will lend this money further at low interest rates. This lending will help to get economic activity back on track to some extent. This, in turn, will help boost economic growth. These efforts of the RBI have been added to the government’s overall economic package.

The RBI, like central banks all across the world, has been trying to flood the financial system with cheap money over the last few months. It has launched several schemes to do so. The names of these schemes are long-term repo operations, targeted-long term repo operations, and targeted-long term repo operations 2.0.

The schemes launched by the RBI lend money to banks at the repo rate, so that they can lend further. The repo rate is the interest rate at which the RBI lends to banks. It was at 5.15 percent and was cut by 75 basis points to 4.4 percent on March 27. These schemes are technically different from one another, but those differences really don’t matter here. What matters is the understanding that the idea is to get banks to lend.

Under these schemes, the RBI has lent a little over Rs 2.38 lakh crore to banks between February 24 and April 23. This money has been lent at the prevailing repo rate. Some part of the lending happened at 5.15 percent and some at 4.4 percent. There are a few other things that the RBI has done to get banks to lend more, including cutting the cash reserve ratio from four percent to three percent. Banks need to maintain a certain proportion of their deposits with the RBI. When this rate is reduced, banks have more money on their books to lend. The cut from four percent to three percent was expected to add Rs 1.37 lakh crore to the financial system, which banks could then lend out.

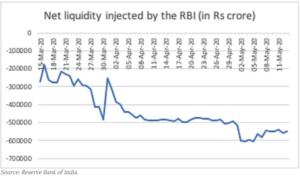

To cut a long story short, the RBI has been trying to flood the system with more money, drive down interest rates, and get banks to lend more. But is that really turning out to be the case? The answer is no. Look at the chart given.

What does the chart suggest? It tells us that the net liquidity injected by the RBI over the last two months has largely been negative territory. As of May 13, this stood at Rs 5.47 lakh crore. What does that mean? It means that RBI’s efforts to inject money into the financial system has been failing massively. As of May 13, 2020, the banks had deposited Rs 5.47 lakh crore with the RBI because of their inability to lend. Banks are unable to lend money due to various reasons. The bad loans of Indian banks, in particular public sector banks, continue to remain high. In the current economic scenario, banks don’t want to lend and accumulate more bad loans, when the ability of many people and businesses to repay loans are dicey. Bad loans are loans which haven’t been repaid for a period of 90 days or more. At the same time, borrowers, even businesses and individuals in a position to repay loans are not in the mood to borrow given the uncertainty that prevails over their economic future.

On the whole, the RBI’s efforts, which are supposed to be a part of the so-called Rs 20 lakh crore economic package of the government, are basically in negative territory of Rs 5.47 lakh crore. Hence, on a lighter note, the size of the government’s economic package is already down to Rs 14.53 lakh crore (Rs 20 lakh crore minus Rs 5.47 lakh crore).

The government’s so-called Rs 20 lakh crore package is a mishmash of various numbers, which shouldn’t be added together in the first place. To put it in simple English, a large part of it is basically a marketing gimmick. Take the case of the rate of the tax deducted at source being reduced. While this does put more money briefly in the hands of people and businesses, it doesn’t reduce the tax outflow in any way.

The government estimates that the move to reduce the rates of tax deducted at source and tax collected at source, will increase the liquidity in the financial system by Rs 50,000 crore. But this is basically money which will continue to be in the hands of people for a slightly longer period of time, until they pay their full and final taxes on this income. How can this be a part of a package or an economic stimulus as the media is calling it?

Also, nowhere in the world have the central bank’s moves to counter the negative impact of the Covid-19 crisis been added to what the government is trying to do. It just doesn’t make any sense. Take the case of the United States. Between February 26 and May 6, the Federal Reserve of the United States has printed and pumped close to $2.6 trillion into the American financial system. The idea, as is the case in India, is to flood the system with money, drive down interest rates, and encourage people and businesses to borrow more.

Over and above this, the US Congress is currently discussing a $3 trillion covid-relief package. No American politician, media house, economist, fund manager, or any other person for that matter has added the two numbers and said that a package of $5.6 trillion ($3 trillion covid relief package and $2.6 trillion printed by the Fed) is being provided to the American citizens.

This is precisely what is happening in the Indian case. This doesn’t make any sense other than coming up with a big round number, which is easy for the government to market and goes very well on WhatsApp forwards, which are the high-definition of truth for most people these days.

www.newslaundry.com